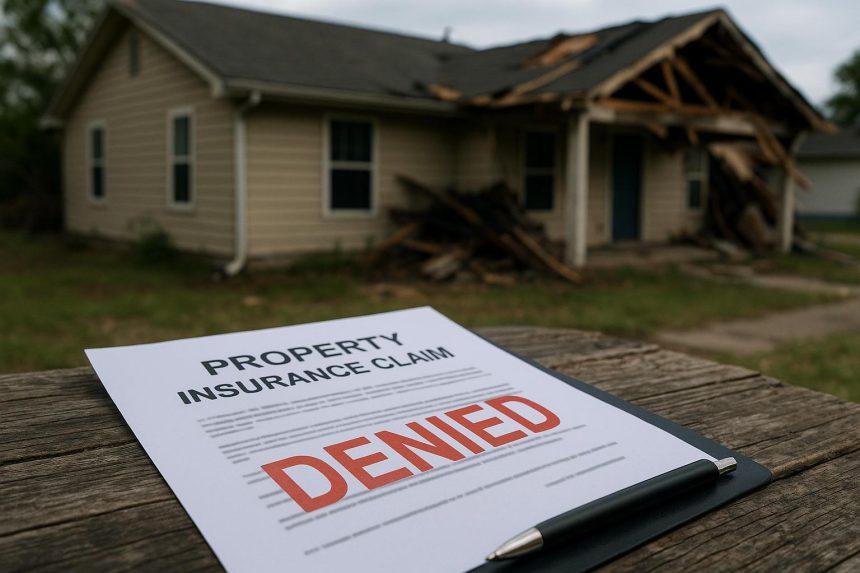

For homeowners and business owners along the Texas Gulf Coast, property insurance is not just a financial product. It is a lifeline. When a hurricane, flood, fire, hail storm, or other disaster strikes, policyholders expect their insurance company to honor the coverage they have been paying for, often for years or decades. But denied and underpaid claims are far more common than most people realize, and when it happens, the financial consequences can be devastating for families and businesses already dealing with the stress of property damage.

Corpus Christi’s location on the Gulf Coast makes it one of the most weather-exposed cities in Texas. The area has been affected by major hurricanes and severe tropical storms, and the insurance claims that follow these events frequently become contentious. Property owners who understand their rights under Texas insurance law are in a far better position to fight back against improper denials and recover the full compensation they are owed.

Why Property Insurance Claims Get Denied in Texas

Insurance companies deny claims for a wide range of reasons, some legitimate and some that fall into the category of bad faith practices. Common legitimate reasons for denial include policy exclusions, lapses in coverage, missed deadlines for reporting damage, or a determination that the damage was caused by something not covered under the policy, such as flood damage under a standard homeowners policy that excludes flood coverage.

However, insurers also deny or underpay claims through tactics that may not hold up under legal scrutiny. These can include misrepresenting the terms of the policy to the policyholder, failing to conduct a thorough and objective investigation of the claim, using biased adjusters or contractors who consistently undervalue damage, unreasonably delaying the claims process to pressure policyholders into accepting less, or applying exclusions in ways that stretch far beyond their intended meaning.

In Corpus Christi and across the Texas Gulf Coast, these issues are particularly acute following major weather events. After hurricanes and severe storms, insurance companies can be overwhelmed with claims and may rush through the adjustment process, leading to significant underpayment or outright denial of valid claims. In some cases, insurers assign adjusters who are unfamiliar with the specific building standards and materials common in the Coastal Bend region, leading to underestimates of repair costs.

Texas Insurance Laws That Protect Policyholders

Texas has some of the strongest bad faith insurance laws in the country, giving policyholders meaningful legal remedies when insurers act improperly. Under the Texas Insurance Code, insurers are required to acknowledge claims promptly, complete investigations within a reasonable time, and pay valid claims or provide a written denial with specific reasons within defined deadlines.

When an insurer violates these requirements, policyholders may be entitled to recover not just the original claim amount but also additional damages, including up to three times the amount of the original claim in cases of knowing bad faith violations, as well as attorney fees and court costs. Texas law also recognizes the common law cause of action for breach of the duty of good faith and fair dealing, which provides an additional avenue for relief when an insurer has no reasonable basis for denying a claim or delays payment without a reasonable basis.

The Texas Prompt Payment of Claims Act imposes specific deadlines on insurers for acknowledging claims, requesting information, and making payment decisions. Violations of these deadlines can result in the policyholder being entitled to interest on the delayed payment at a rate of 18% per year, which is a meaningful financial penalty designed to discourage delay tactics.

The Role of a Property Insurance Claims Lawyer

Navigating a disputed insurance claim without legal representation puts policyholders at a significant disadvantage. Insurance companies have teams of adjusters, attorneys, and claims specialists whose job is to minimize payouts. Having an attorney who understands Texas insurance law and knows how to build a compelling case levels the playing field considerably.

A property insurance claims lawyer will begin by conducting an independent review of your policy to determine exactly what coverage you are entitled to. They will then work with independent adjusters and damage experts to establish the true extent and value of your losses, compare that assessment against what the insurer has offered, and identify any violations of Texas insurance law that may entitle you to additional damages beyond the original claim amount.

“Too many Corpus Christi homeowners accept a denial or a lowball offer because they do not know they have options,” says a representative from Carrigan Anderson. “A Corpus Christi property insurance claims lawyer can review your policy, challenge the insurer’s decision, and fight for every dollar of compensation you are owed under your coverage. The insurance company has professionals working for them. You deserve the same.”

Steps to Take After a Claim Denial in Corpus Christi

If your property insurance claim has been denied or you believe you have been significantly underpaid, there are several important steps to take as soon as possible. First, request a written explanation of the denial and review it carefully against the terms of your policy. Insurers are required by Texas law to provide specific reasons for any denial, and vague or general explanations may themselves be a violation of Texas insurance law.

Second, document all damage thoroughly with photographs, videos, and written records. If you have already begun repairs out of necessity, keep all receipts and contractor invoices as evidence of the scope of damage. Third, do not accept a settlement offer without consulting an attorney. Once you accept a settlement and sign a release, you may forfeit your right to seek additional compensation, even if you later discover the payment was far below what you were owed. Texas has a two-year statute of limitations for most insurance claim disputes, making prompt action essential.

Lynn Martelli is an editor at Readability. She received her MFA in Creative Writing from Antioch University and has worked as an editor for over 10 years. Lynn has edited a wide variety of books, including fiction, non-fiction, memoirs, and more. In her free time, Lynn enjoys reading, writing, and spending time with her family and friends.