Martin J. Milita brings decades of legal, regulatory, and business leadership to questions of corporate acquisition and risk. As senior director of Duane Morris Government Strategies (DMGS), an affiliate of the international law firm Duane Morris LLP, he advises Fortune 500 companies, public agencies, and private enterprises on government relations, regulatory compliance, and crisis communications. Earlier in his career, he served as CEO of Fiore Group Companies, Inc., overseeing solid waste operations across eleven New Jersey counties, and as a managing partner at Holman Public Affairs LLC, where he helped clients navigate complex legislative and procurement environments. His background as an attorney at law, combined with nearly a decade as chief deputy attorney general with the New Jersey Department of Law and Public Safety, gives him direct experience with the compliance, regulatory, and operational factors that determine whether a business acquisition succeeds or fails after closing.

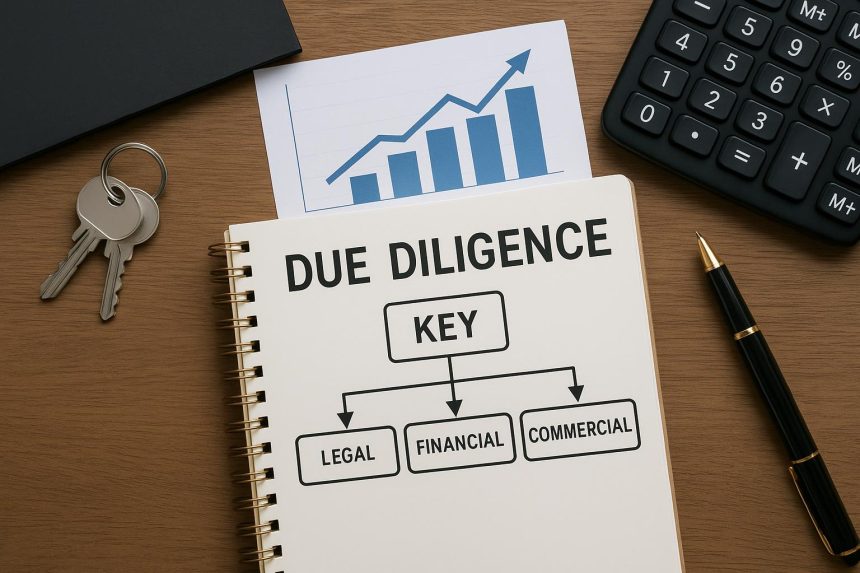

Businesses often buy other companies to grow faster, enter new markets, or add capabilities they do not already have. That strategy only works when the target company can keep operating the way the buyer expects after closing. In plain terms, due diligence means testing the target's records, obligations, approvals, and operating risks before the buyer commits.

The financial review usually comes first because it tests whether the business has actually performed the way the seller claims. A buyer should examine financial statements, tax filings, cash flow, debt, and unusual swings in revenue or expense instead of relying on a presentation. A buyer should also test revenue quality, because strong sales can still be fragile when too much income comes from one customer, one contract, or one temporary spike in demand.

Contracts matter because they define duties the buyer may have to carry after the sale. Customer agreements, vendor terms, leases, loan documents, and service commitments can shape what the company must keep doing once ownership changes. A buyer also needs to watch for change-of-control clauses, which may let the other party cancel, refuse consent, or renegotiate after a sale.

Past legal or compliance trouble creates a different kind of risk. Lawsuits, threatened claims, settlements, audits, investigations, and prior enforcement actions can point to costs or restrictions that have not fully surfaced yet. The question is not only what the company must do after closing. It is also what problems may still emerge after the purchase.

That question becomes even more important in regulated industries, and healthcare provides a clear example. A buyer may need to examine provider enrollment, billing practices, reporting duties, ownership-change filings, and prior compliance problems because the business can lose revenue if the company fails to complete required billing or enrollment updates. More broadly, some businesses face post-closing disruption because ownership-related regulatory steps interrupt normal operations.

A buyer should review licenses, permits, and operating approvals separately because current authority does not always transfer automatically to a new owner. A buyer should confirm that the target holds the approvals it needs, that those approvals remain current, and that the business can renew, transfer, or update them after the sale. In some industries, a company can keep its customers and staff yet still face shutdown risk if a required permit or approval does not carry over cleanly.

Daily operations may depend too heavily on a few employees or managers. Some businesses rely on one owner's judgment, one manager's relationships, or a small group of employees who know how to handle scheduling, customer issues, or compliance steps. Operational records also matter because a buyer should see how the company tracks deadlines, stores contracts, documents decisions, handles reporting, and maintains organized files.

Consistent systems make it easier to tell whether the business runs through repeatable processes instead of memory or improvisation. Once the buyer identifies financial, legal, regulatory, and operational issues, those findings should shape the deal itself. A careful review may justify a lower price, stronger seller promises, indemnity protection, other buyer protections, transition support, or closing conditions that the seller must meet. In some cases, the most disciplined decision is to walk away.

Due diligence gives the buyer a stronger basis for deciding whether the business can keep functioning as expected after the sale closes. It helps separate a company that only looks attractive on paper from one that can continue operating under new ownership. That is what makes the review valuable before the buyer commits.

About Martin J. Milita

Martin J. Milita is an attorney at law and senior director of Duane Morris Government Strategies (DMGS), affiliated with the international law firm Duane Morris LLP. He previously served as CEO of Fiore Group Companies, Inc. and as managing partner of Holman Public Affairs LLC. Earlier in his career, he held the role of chief deputy attorney general with the New Jersey Department of Law and Public Safety. He earned his JD from Temple University School of Law.

Lynn Martelli is an editor at Readability. She received her MFA in Creative Writing from Antioch University and has worked as an editor for over 10 years. Lynn has edited a wide variety of books, including fiction, non-fiction, memoirs, and more. In her free time, Lynn enjoys reading, writing, and spending time with her family and friends.